Position in Rating | Overall Rating | Trading Terminals |

100th | 2.0 Overall Rating |

|

M1 Finance Review

M1 Finance is positioned as an all in one money platform that combines investing, cash management, and borrowing in a single app experience. On its official site, M1 highlights automated investing, commission-free investing tools, cash accounts, and portfolio-backed borrowing, which makes it stand out for people who want a more hands-off approach. M1 Finance is not a traditional advisor and does not provide personalized investment guidance. Unlike a financial advisor, M1 offers automation and portfolio customization but does not provide professional advisory services.

For this M1 Finance Review, the first thing worth noting is that M1 is not just a basic stock app. The platform supports multiple account types, including individual and joint brokerage accounts, custodial accounts, IRAs, trusts, and crypto, which gives it a wider reach than many beginner platforms.

A truthful introduction also needs the fine print. M1 states that investing involves risk, brokerage products are not FDIC insured, and while self-directed brokerage accounts do not have commission, trading, or management fees, users may still face other charges like a platform fee and regulatory fees depending on account status. Account fees, such as annual, inactivity, or closing fees, may apply depending on the account type. Additionally, a monthly fee may apply for certain account types or balances.

What is M1 Finance?

M1 Finance is a financial platform that combines investing, cash features, and borrowing tools under one brand, rather than offering only a basic stock trading app. On its official site, M1 describes itself as a technology company with separate affiliates that handle different parts of its services, which is important for readers who want to understand how the platform is structured.

In simple terms, M1 is best known for automated investing and self-directed brokerage accounts, where users can manage portfolios without commission, trading, or management fees on those accounts. While M1 offers automation tools similar to a robo advisor, it is not a traditional robo advisor because it lacks full automation and advisory services, making it more suitable for experienced investors who value customization. That said, M1 also clearly discloses that users may still pay other charges, including a platform fee and regulatory fees, so it is not accurate to call it completely free.

A key point in this M1 Finance review is that M1 is not a bank, even though it offers cash-related products and lending services. M1 states that some banking and lending services are furnished by B2 Bank NA, while brokerage services are provided by M1 Finance LLC, which is listed as an SEC-registered broker-dealer and FINRA/SIPC member. Cash deposits are held at a partner bank, which provides FDIC insurance coverage for those funds. Additionally, brokerage accounts are protected by SIPC insurance, which covers investments against brokerage firm failures up to certain limits, but does not protect against market losses.

M1 also makes it clear that all investing carries risk, including the possibility of losing money, and that borrowing through margin can increase those risks. Margin accounts allow users to borrow against their portfolio and are subject to specific interest rates, which should be carefully considered before using leverage. For general users, that means M1 is built for convenience and long-term money management, but it still needs the same level of care and risk awareness as any other investing platform.

Benefits of Trading with M1 Finance

One of the biggest benefits of using M1 Finance is its focus on automated investing with a simple long term setup, designed to meet the needs of customers seeking long-term investing solutions. M1 lets users build a portfolio, set target allocations, and use auto-invest features so money is directed into the portfolio without manual trade-by-trade work.

Another strong advantage is the platform’s customization and account variety. M1 supports individual, joint, custodial, retirement, trust, and crypto-related options, which makes it easier for users to manage different goals in one ecosystem instead of splitting everything across multiple apps. Customers can invest in fractional shares, allowing them to build diversified portfolios regardless of account size. Users access a range of account types and features through a single platform, streamlining investment management.

M1 also combines investing with cash and borrowing tools, which is useful for users who want one platform for more than just buying stocks or ETFs. On the official site, M1 highlights high-yield cash features and a portfolio line of credit, including margin borrowing that can reach up to 50% of portfolio value for eligible accounts.

The honest downside is that M1 is not truly zero-cost for everyone, even though self-directed brokerage accounts do not charge commission, trading, or management fees. Smaller accounts may be subject to a monthly fee, while larger accounts may qualify for fee waivers. M1 discloses a monthly platform fee in certain cases, and it also notes that regulatory and other account-related fees may still apply, so users should check the fee rules before opening an account.

A final benefit for some users is the platform’s hands-off portfolio maintenance style, especially through dynamic rebalancing. M1 states that underweight holdings are bought first based on the targets set by the user, which helps keep a portfolio aligned over time without constant manual adjustments.

M1 Finance Regulation and Safety

When reviewing M1 Finance regulation and safety, the first thing to understand is that M1 operates through separate entities, and the brokerage side is handled by M1 Finance LLC. M1’s disclosures state that brokerage products are offered by M1 Finance LLC, which is an SEC-registered broker-dealer and a member of FINRA and SIPC, providing SIPC insurance for securities held in brokerage accounts.

M1 also makes an important distinction that many users miss, which matters for safety expectations. The company states that M1 is not a bank, and brokerage products are not FDIC insured, not bank guaranteed, and may lose value.

For cash-related products, the protection depends on where funds are held. M1 explains that funds in a brokerage account are protected by SIPC, while participating cash balances, including uninvested cash, may be swept to partner banks in the deposit network to become eligible for FDIC insurance coverage.

M1’s risk disclosures are also clear that investing and borrowing are not risk-free, even on an automated platform. Its legal disclosures state that all investing involves risk, and using margin through M1 Borrow can increase risk further.

In March 2024, FINRA announced an $850,000 fine against M1 Finance related to social media influencer promotions, including issues around unfair or misleading communications and supervision, and FINRA said M1 agreed to remediate the issues as part of the settlement.

Overall, M1 shows strong transparency in its disclosures, which is a positive sign for users checking broker safety. At the same time, the platform still carries normal market risk and has a public enforcement record, so users should treat it as a regulated broker platform, not a guaranteed-safe savings app.

M1 Finance Pros and Cons

Pros:

- Automated investing tools help users invest without placing every trade manually through Auto-invest and target-based portfolio management.

- Custom Pies make it easier to build and manage personalized portfolios with adjustable allocations.

- Commission-free self-directed investing is a real advantage for users focused on reducing trading costs.

- Dynamic rebalancing behavior helps keep portfolios closer to target weights over time by buying underweight slices first.

- All-in-one money features combine investing, cash accounts, and borrowing in one ecosystem.

- Portfolio line of credit access can provide liquidity without selling investments for eligible accounts.

- Multiple account types support different needs, including individual, joint, custodial, and retirement-focused setups.

Cons:

- A monthly platform fee may apply if account requirements are not met, so it is not fully free for everyone.

- M1 is a self-directed platform, which may not suit users who want personal investment advice or guided planning.

- Brokerage products are not FDIC insured and can lose value, so users still carry normal market risk.

- Margin borrowing can increase losses if investments move the wrong way, even though it adds flexibility.

- M1 is not a bank, which can confuse users expecting a traditional checking or savings setup.

- The high-yield cash account is an investment product and requires an open M1 Invest account to participate.

- Crypto access is handled through separate entities, and crypto assets are not FDIC or SIPC insured.

M1 Finance Customer Reviews

Customer reviews for M1 Finance show a mixed to negative public sentiment on Trustpilot, while M1’s own website highlights strong mobile app ratings and growth metrics. This review is based on hands on testing of the M1 Finance platform, including direct interaction with its features and user interface, to provide an informed perspective on its functionality and user experience. This matters in a broker review because it shows two different angles: the company’s official performance claims and the complaints users post on third-party review platforms.

On Trustpilot, the M1 profile shows a low overall score with more than 200 reviews, and the page labels the rating as Bad. The review breakdown also shows that 1-star reviews make up the largest share, which is a clear warning sign for users researching customer experience before opening an account.

A closer look at Trustpilot comments shows repeated complaints about withdrawals, transfer setup issues, fees, and customer support quality. Some recent posts also include unusual recovery-service language, so readers should treat individual reviews carefully and focus more on repeated patterns than on any one post.

It is also important to note that Trustpilot itself says it does not fact-check specific claims, and that reviews are user opinions. Trustpilot also notes this M1 profile includes merged reviews from one or more profiles, which can affect how readers interpret the full history of the rating.

On the official M1 website, the company presents a much stronger picture, including 4.7 on the Apple App Store, 4.5 on Google Play, more than 1,000,000 users, and over $12B in client assets as of September 2025. These figures suggest the platform has scale and active usage, even though public review sites still reflect customer frustration in key service areas.

For this review, the takeaway is that M1 appears strong on product adoption and app usability, but its customer review reputation on Trustpilot remains a weak point. That does not automatically mean the broker is unsafe, but it does mean users should pay close attention to fees, transfer processes, and support responsiveness before funding an account.

Account Types

Individual Brokerage Account

Standard investing account for one person with access to stocks and ETFs, plus M1’s automated portfolio tools and custom Pies. Individual brokerage accounts on M1 also allow users to invest in fractional shares of stocks and ETFs, making it easier to fully invest available funds and build diversified portfolios. M1 positions this as a self-directed account for long term investing with commission-free trading on eligible self-directed brokerage activity.

Joint Brokerage Account

Shared investing account for two owners, often used by couples or family members with shared financial goals. M1 states both owners can contribute, withdraw, and make portfolio changes, which is a useful feature for joint planning.

Custodial Account

Minor-focused investment account where an adult custodian manages assets on behalf of a child until the age of majority. M1 explains that the account is taxable and the assets transfer to the minor when they reach the required age under state rules.

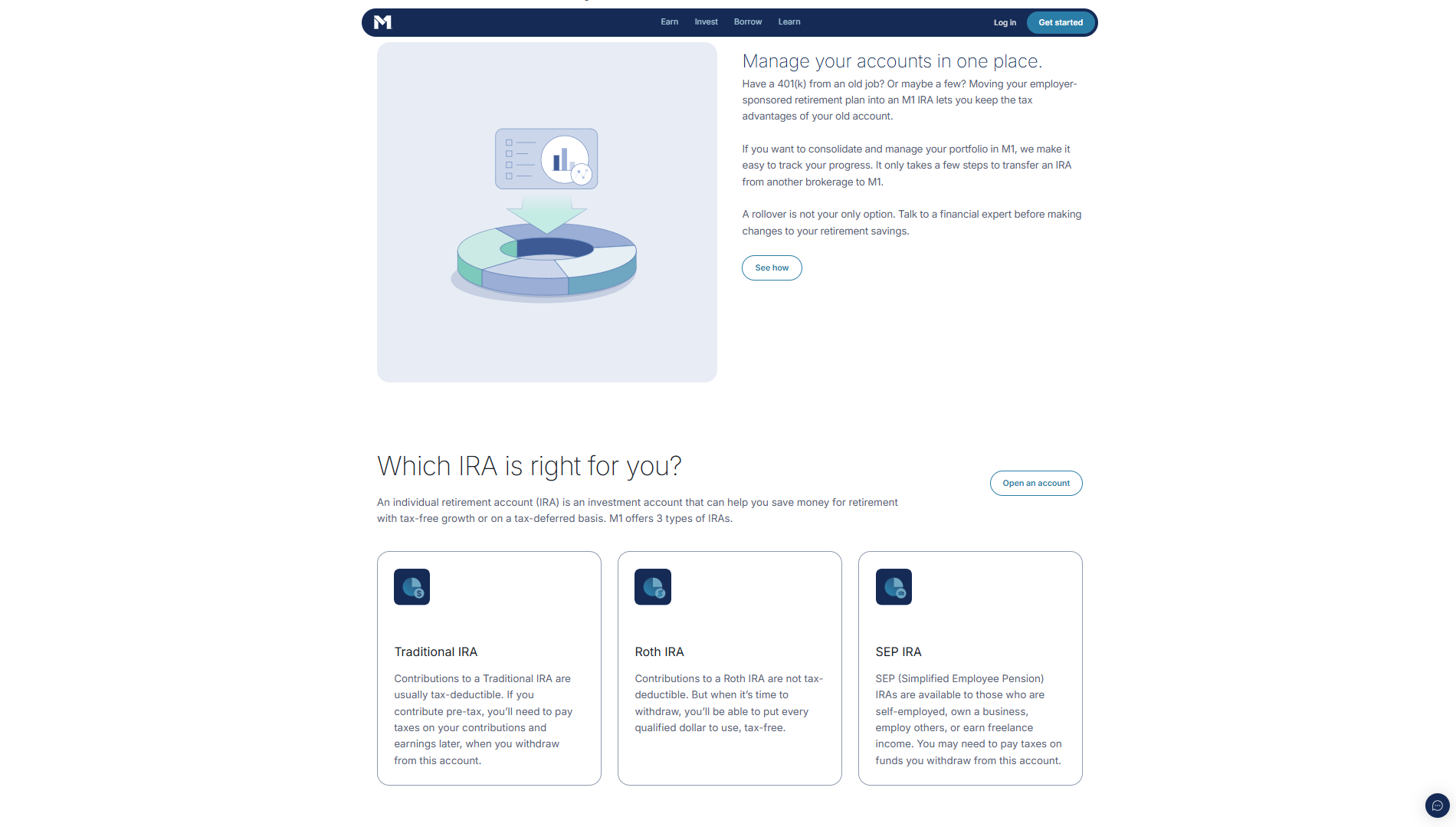

Traditional IRA

Retirement account designed for long term retirement investing with M1’s self-directed and automated investing tools. M1 lists Traditional IRA as one of its core IRA options under its retirement accounts lineup.

Roth IRA

Tax-advantaged retirement account option for users building long term retirement savings through M1’s investment platform. M1 includes Roth IRA in its retirement account offerings and supports automated portfolio management inside IRA accounts.

SEP IRA

Retirement account for self-employed users and eligible small business situations, offered as part of M1’s IRA lineup. M1 includes SEP IRA on its retirement page, making it a relevant option for users who need a business-friendly retirement account type.

Trust Account

Estate and legacy planning account for eligible trusts that want to invest in securities through M1. M1 states it supports both revocable and irrevocable U.S. domestic trusts in good legal standing, and it lists a minimum account value requirement for trust accounts.

Crypto Account

Crypto investing account that lets funded M1 Invest users buy and manage supported cryptocurrencies, including Crypto Pies and dynamic rebalancing. M1 also notes crypto services are provided through Bakkt and that crypto holdings are not FDIC or SIPC insured.

Cash Account

High-yield cash account option is also part of the broader M1 ecosystem, but M1 notes it is an investment product and not a traditional bank checking or savings account. M1 also states an open M1 Investment account is required to participate in the high-yield cash account program.

How to Open Your Account

- Get started

Go to the official M1 website and click Get started to begin the application. M1 links this directly to its account sign-up flow from the homepage and Help Center. - Check if you meet the eligibility rules

M1 says applicants must be a U.S. citizen or permanent resident, be at least 18 years old, have a current U.S. residential address, and have a valid U.S. phone number. M1 also notes that VOIP numbers are not accepted for verification. - Choose your first account type

M1 states that every client must first open an Individual Brokerage Account or an IRA before opening more account types. It also notes that if an IRA is the first account, that first IRA setup can only be opened on web.

For example, if your goal is to invest for retirement, you might choose an IRA to take advantage of tax benefits. If you want more flexibility and access to your funds, an Individual Brokerage Account could be a better fit. This helps illustrate how M1 lets users tailor their account type to their specific investing strategy.

- Fill out and submit the application

Complete the account application form with your personal details and submit it through the M1 sign-up flow. M1 says this is the official step that starts the review process for account approval. - Prepare your verification details and documents

M1 says identity can often be verified automatically, but sometimes extra documents are required. If needed, M1 may request proof of identity, proof of address, and your Social Security Number for tax reporting and verification. - Watch for M1’s email update

M1 says applicants usually receive an email within one business day confirming approval or requesting more information. If documents are requested, M1 includes secure upload instructions in that email. - Wait for review if extra documents are needed

If M1 requests documents, the Help Center says review can take about 5 to 7 business days after the documents are submitted. This is a normal compliance step and not unusual for regulated financial platforms. - Fund your account after approval

Once approved, the next step is to fund the account and begin setting up your investments. M1’s account guides also show minimum opening amounts for some account types, such as $100 for many brokerage, custodial, and crypto accounts, and $500 for IRA accounts. - Add more account types if needed

After your first account is completed, M1 allows additional eligible accounts such as Joint, Custodial, Trust, Cash, and Crypto accounts. M1 also notes that new account types may take up to 24 hours to become available in your dashboard.

M1 Finance Trading Platforms

M1 Finance offers a multi-platform experience through its web platform and mobile app, which is useful for users who want to manage investing, cash, and borrowing in one place. M1’s terms also confirm that the “M1 Platform” includes both its website and the M1 mobile app, so users can expect the same core ecosystem across devices.

On M1’s official site, the platform is positioned as flexible, customizable, and automated, with a strong focus on long term investing instead of constant manual trading. That makes M1 a better fit for portfolio builders than for traders looking for fast intraday execution tools.

The web platform is the main place where M1 organizes account setup, portfolio management, and account type options such as brokerage, retirement, trust, and crypto. M1’s Help Center also notes that its quick-start guide focuses on the web experience, which suggests the browser version remains a core part of the platform workflow.

For mobile users, M1 is available on both iOS and Android, and the company presents the app as an all in one finance app for earning, investing, and borrowing. M1’s Help Center specifically says the same features can be used on the app, which is a practical advantage for users who want to manage portfolios from a phone.

A key platform feature in this M1 Finance review is the automation system behind trading activity. M1 states that it uses a proprietary trading system where buys are queued and executed during specific trading windows, which may limit the timing of order execution, so users do not need to manually place every trade if they do not want to.

M1’s trading platform also includes tools that support portfolio management, not just order entry. On its brokerage page, M1 highlights dividend handling options like DRIP and portfolio-level reinvestment, plus performance tracking against stocks, ETFs, and custom Pies. However, M1 Finance provides limited market research tools compared to some other platforms, which may affect users seeking in-depth data and analysis for investment decisions.

The honest downside is that M1’s platform design may feel limiting for users who want real-time trading control or a classic active-trader terminal. Its automated trade window system is simple and efficient for long term investing, but it is not built like a professional day trading platform with advanced charting and rapid order routing.

Overall, M1 Finance trading platforms are strongest for users who want automation, portfolio customization, and a clean web and mobile setup in one place. For active traders, the platform may feel too structured, but for long term investors, that same structure can be one of M1’s biggest strengths.

What Can You Trade on M1 Finance

M1 Finance is built mainly for long term investing, so the platform focuses on a narrower list of assets than a full active trading broker. Based on M1’s official pages and Help Center, users can trade U.S.-listed stocks, ETFs, and a curated list of cryptocurrencies through eligible accounts.

For standard investing accounts, M1 supports U.S.-listed stocks and ETFs from major exchanges like NYSE and Nasdaq. This is the core of the M1 platform, and it fits users who want to build custom portfolios or “Pies” using stocks and ETFs with automated investing tools. Users can implement various investment strategies, such as passive investing, growth investing, or value investing, by customizing their Pies and choosing from different Model Portfolios.

M1 also offers crypto investing through a separate Crypto Account for eligible users who already have a funded M1 Brokerage Account. On its crypto page, M1 lists supported coins such as Bitcoin, Ethereum, Solana, XRP, Cardano, and others, and it notes that crypto services and custody are provided through Bakkt.

Another important detail for this M1 Finance review is what the platform does not support. M1’s Help Center states that mutual funds, options, and OTC securities are not supported, which may be a downside for users who want more advanced or speculative trading products.

M1 also mentions that users can get indirect crypto exposure through certain crypto-related assets inside brokerage accounts or IRAs, such as blockchain-related ETFs. This gives users more flexibility if they want crypto-themed exposure without holding only spot crypto positions.

When it comes to liquidation, users can sell assets as part of portfolio rebalancing or when withdrawing funds. The platform facilitates buying and selling assets to maintain a target allocation, supporting long-term investing without frequent manual intervention.

The takeaway is that M1 works well for users who want stocks, ETFs, and crypto in one automated platform, but it is not designed for everything. If the goal is options trading, mutual fund investing, or OTC stock trading, M1 will likely feel limited.

M1 Finance Customer Support

M1 Finance customer support is centered on its Help Center, Messenger chat, email support, and phone support, with most support paths pointing users to the official M1 Help Center first. M1 also promotes its Client Success Center on the main site for product questions and account guidance.

On the M1 Help Center Contact Us page, M1 says the fastest response is through Messenger. Existing clients are directed to log in and use the “Help” option on web or “Client Support” on mobile, while general visitors can use the chat bubble in the lower right corner of the Help Center.

M1 also provides direct phone and email support for users who prefer traditional contact options. The Contact Us page lists the support phone number as 312-600-2883 and shows separate emails for login help, securities lending, and other requests.

For support availability, M1 states its Client Success team is usually available on days when the U.S. stock market is trading, and it also lists phone support hours as Monday through Friday from 9 am to 4 pm ET, excluding market holidays. This is a helpful detail for users because it sets clear expectations and shows support is not positioned as 24/7.

A useful support feature for beginners is the structured Help Center, which is organized by account management, money movement, investing, borrowing, and other common topics. This makes self-service easier before contacting support, especially for routine tasks like transfers, funding, and account setup.

The downside is that support appears to rely heavily on chat and standard business-hour availability, which may feel limited for users who want instant help late at night or on weekends. Still, M1 does provide multiple official contact routes and clear guidance on where to go for the fastest response.

M1 Finance Customer Support Advantages and Disadvantages

Withdrawal Options and Fees

M1 Finance offers several ways to move money out, but the best option depends on whether the withdrawal is cash, a bank transfer, or a full account transfer. For most users, the main withdrawal routes are ACH transfers to a linked bank, wire transfers, and full account liquidation to a bank.

A normal cash withdrawal is usually done through M1’s transfer tools by moving money from an eligible M1 account to a connected external bank account. M1’s account agreement also notes ACH withdrawal timing can take a few business days, so it is not always instant. Uninvested cash balances in your account may earn interest, and if you use margin loans, those are subject to interest charges.

For faster movement, M1 supports wire transfers for eligible accounts. M1’s Help Center states outgoing wires carry a $25 fee, while incoming wires have a $0 M1 fee, although the sending bank may still charge its own fee.

M1 also provides a liquidation withdrawal option if a user wants to close out an investment account and send the full cash value to a linked bank. The Help Center explains this process sells all positions first, and then transfers the proceeds, which is important because it may trigger taxes and it cannot be reversed once confirmed.

If the goal is to move investments to another broker instead of withdrawing cash, M1 supports outgoing ACAT transfers. M1 states there is a $100 outgoing ACAT fee for all account types, and retirement accounts can face an additional $100 closing fee, which makes IRA transfers out more expensive.

A point for this review is that M1’s fee structure is not only about withdrawals. M1 also discloses platform and IRA fees in some cases, plus regulatory fees on certain sales, so users should check the fee pages before moving money or closing accounts.

Overall, M1’s withdrawal options are practical and clearly documented, but users should pay attention to timing, wire fees, and transfer-out fees before making a move. This is especially important for larger withdrawals or full account transfers where fees and processing steps can affect the final amount received.

M1 Finance Vs Other Brokers

#1 M1 Finance vs. AvaTrade

AvaTrade is built for active trading and CFD markets, with a much wider product lineup that includes forex and CFDs on commodities, stocks, ETFs, bonds, crypto, and indices. It also promotes broad oversight, stating it is regulated across 9 jurisdictions and listing regulators such as the Central Bank of Ireland, CySEC, and other regional authorities on its regulation page.

M1 Finance is very different in how it is designed and who it serves. M1 focuses on long term investing with automated portfolio tools, commission-free self-directed brokerage investing, and account types like individual, joint, custodial, IRA, crypto, and trust accounts, which makes it more of a portfolio-building platform than a fast-trading terminal.

Verdict: AvaTrade is a better fit for users who want broad CFD market access and stronger multi-region regulation visibility, while M1 Finance is better for users who want automated investing and a simpler long term portfolio experience.

#2 M1 Finance vs. RoboForex

RoboForex is positioned as a multi-asset trading broker with a much larger trading catalog and a more trader-focused setup. On its official pages, RoboForex says it offers more than 12,000 instruments across 7 asset types, supports platforms like MT4, MT5, and R StocksTrader, and provides contract specifications with spreads, commissions, and trading conditions by account type.

M1 Finance is narrower but more streamlined for investors who want portfolio automation instead of high-frequency execution tools. M1’s strength is in automated stock and ETF portfolio management, custom portfolio allocation, and integrated account options, while RoboForex is structured more for leveraged trading and platform variety.

On regulation and risk profile, RoboForex discloses FSC Belize regulation, Financial Commission membership, and a risk warning that a large percentage of retail CFD accounts lose money, which is a very different environment from M1’s self-directed investing model. M1 also carries market risk, but its official disclosures frame the platform around investing and wealth management rather than leveraged CFD speculation.

Verdict: RoboForex suits users who want more instruments, more trading platforms, and leveraged CFD-style trading, while M1 Finance suits users who prefer automated investing and a cleaner long term approach.

#3 M1 Finance vs. Valetax

Valetax presents itself as a trading-focused broker with 100+ financial instruments and account types aimed at different trading styles, including Cent, Standard, and ECN accounts. Its site also highlights tradable categories like indices, metals, crypto, and energies, with promotional language around zero-commission conditions on some instruments.

M1 Finance is a better comparison if the user wants a portfolio platform instead of a classic CFD broker layout. M1 emphasizes automated investing, brokerage and retirement account types, and a simpler investment ecosystem rather than offering multiple spread-based trading account models like Cent or ECN.

In terms of regulation, Valetax discloses on its site that Valetax International Limited is authorized and regulated by the Mauritius FSC. That is a legitimate disclosure, but M1’s structure is different because its brokerage services are offered by M1 Finance LLC, which M1 states is an SEC-registered broker-dealer and FINRA/SIPC member.

Verdict: Valetax is more suitable for users looking for forex/CFD-style account options and short-term market trading, while M1 Finance is more suitable for users focused on automated, long term investing with a simplified account structure.

Also Read: AvaTrade Review 2024- Expert Trader Insights

OPEN AN ACCOUNT WITH M1 FINANCE

Conclusion: M1 Finance Review

M1 Finance is a strong choice for users who want automated investing, portfolio customization, and a simple all in one setup for investing, cash, and borrowing. On its official site, M1 clearly positions itself around long term investing instead of fast manual trading, which makes it a better fit for investors than for active day traders.

A big strength in this M1 Finance review is the platform’s focus on ease of use and account flexibility. M1 supports multiple account types, offers commission-free self-directed brokerage investing, and includes tools like portfolio automation and built-in borrowing features that can be useful for long term users.

The main tradeoff is that M1 is not fully “free” for every user, and it is not built for advanced short term trading workflows. M1 discloses a monthly platform fee in some cases, plus other possible fees, and its platform structure is centered on managed investing behavior rather than real-time active trading tools.

From a safety and structure standpoint, M1 presents itself with clear disclosures, including SIPC membership for brokerage protections and FDIC-related coverage details for eligible cash deposits through partner banks. It also clearly states that M1 is not a bank and that investing still carries risk, which is an important point for general users.

The final verdict is that M1 Finance is a good platform for people who want a hands-off investing experience and a cleaner way to manage money in one app. It is less suitable for traders who need broad asset classes, advanced charting, or high-speed execution, but for long term portfolio building, M1 remains a competitive option.

M1 Finance Review: FAQs

Is M1 Finance a legit broker or investment platform?

M1 Finance’s website lists a physical office address, support email, and states that M1 Finance Investment operates as a subsidiary of M1 Finance Asset Management, with a published FINRA number (164193) and SEC number (801-115048). Those details are useful for basic verification, but users should still check official regulator databases and read the legal terms before depositing larger funds.

What can you invest in on M1 Finance?

On its homepage and education pages, M1 Finance presents itself as a multi-asset platform and mentions products like stocks, options, crypto, bonds, and ETFs, with separate sections for cash, automated investing, crypto investing, and bond investing. This makes M1 Finance more of an all-in-one investing platform than a single-asset broker.

How do you open an M1 Finance account?

M1 Finance’s onboarding flow is shown as Sign Up, Fund, and Buy, and the “How to Invest” page adds that users should complete the application, verify the account with an ID, and deposit into the cash account before investing. The site also says to contact support if the correct application form is not visible during signup, which is helpful for users opening a specific account type.

OPEN AN ACCOUNT NOW WITH M1 FINANCE AND GET YOUR BONUS